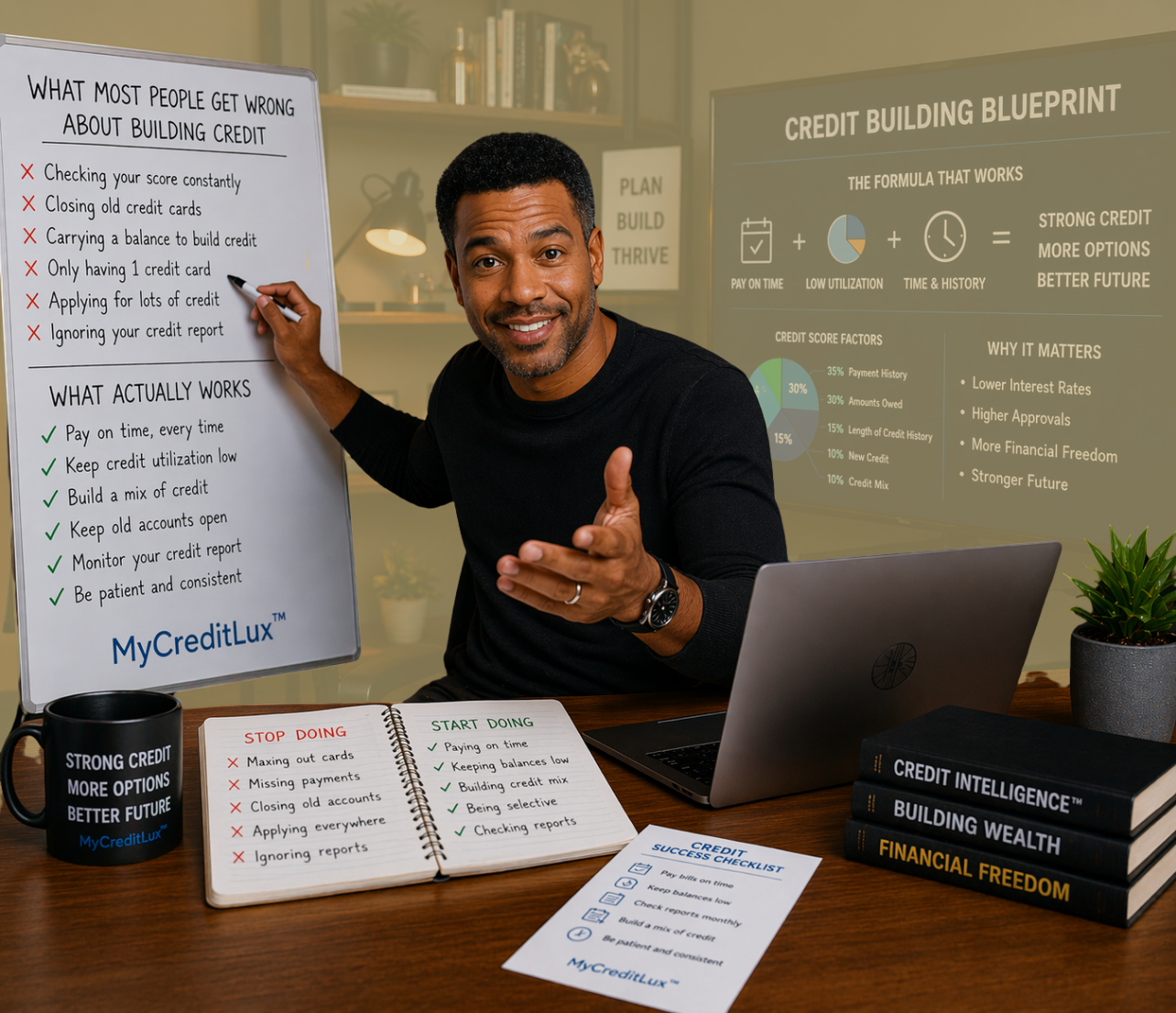

Key Takeaways

- Scores move on reported behavior, not intentions—timing and balances at statement cut date matter.

- Low revolving utilization across each card beats paying after the fact.

- Age, limit depth, and clean payment streaks compound; closing old cards stalls growth.

- Lenders use more than your score: income stability, recent inquiries, and internal data shape approvals and limits.

- Targeted fixes beat blanket disputes; accuracy and persistence win.

How credit actually reports

Most issuers report your statement balance, not the balance after you pay on the due date. If the number that hits the bureaus is high, your utilization spikes even if you later pay in full. That gap confuses many people.

Mechanism

Revolving utilization = statement balance ÷ credit limit, evaluated per card and in total. Scoring models react most between 1–9% (strong), 10–29% (okay), 30–49% (pressure), 50–89% (stress), 90%+ (risk). Payment history is binary: on time or late, with 30/60/90+ day buckets increasing damage.

Lender view

Underwriters look past your score to see utilization trends, new account velocity, credit line depth, and any recent late payments. They compare this with income and internal behavior (prior limits, cash flow, relationship history) to size limits and price risk.

What people get wrong—and what to do

1) Paying only by due date

Fix: Pay early to control what reports. Set an “internal” pay date 2–3 days before the statement cut so the reported balance is low and predictable.

2) Chasing zero balances everywhere

Models often prefer at least one card to report a small balance while others report $0. A thin file with all $0 can look inactive. Let one card report a small, planned charge; pay it the day after it posts.

3) Closing old, fee-free cards

Age and available limit support your score and approvals. Keep no-annual-fee cards open to preserve history and capacity unless there is a clear reason to close.

4) Opening too much, too fast

Each hard inquiry and new line reduces average age and can trigger bank risk thresholds. Space applications 3–6 months apart while building clean on-time streaks.

5) Disputing everything

Dispute only inaccurate or unverified items with documentation. Frivolous disputes waste time and can backfire; goodwill and pay-for-delete (where allowed) work best when supported by facts.

Execution checklist

- Autopay minimums everywhere to eliminate accidental lates; manual early pay to manage utilization.

- Target per-card utilization under 9% and total under 9–14% for steady gains.

- Use 2–3 primary cards for activity; keep others at $0 and open.

- Add one well-chosen secured or entry card if thin; graduate it by keeping $0 lates and low utilization for 6–12 months.

- Recheck reports monthly; correct only what is wrong and document everything.

Benchmarks and examples

Use these conversions to translate habits into data lenders and bureaus actually see.

How Activity Actually Reports vs What People Assume| Action | What People Assume | What Bureaus/Lenders See |

|---|

| Pay on due date after statement | Low utilization will show | High statement balance already reported; score reflects spike |

| All cards at $0 | Maximum score | Thin file may look inactive; one small balance can score better |

| Close old no-fee card | Cleaner wallet, no downside | Lower total limits and age; approval odds and limits can drop |

| Open 3 cards in 30 days | Fast build | High velocity and inquiries; internal risk flags, lower starting limits |

| Dispute accurate late | It will vanish | Verified data remains; time and new positive history matter more |

Utilization Math You Can Control| Card Limit | Target 9% | Risk Zone 30%+ | Reporting Move |

|---|

| $500 $45 $150+ Pay to $20—$40 two days before cut $150+ $45 | | | |

| $1,500 $135 $450+ Split spend across cards; schedule early payment $450+ $135 | | | |

| $5,000 $450 $1,500+ Keep big purchases off cycle; use 2 payments per cycle $1,500+ $450 | | | |

| $10,000 $900 $3,000+ Pre-pay large charges; avoid single-card spikes $3,000+ $900 | | | |

Timeline: What Changes First| Change | When You See It | Why |

|---|

| Lower utilization | Next statement after early pay | New, lower balances are what report |

| Remove an error | 30—45 days post-dispute CRA investigation window | |

| Add new card | Immediate small dip; 3—6 months stabilize | Inquiry + new line; age grows back |

| On-time streak | 3—12 months Payment history weight compounds with time | |

Timeline: What Changes First| Change | When You See It | Why |

|---|

| Lower utilization | Next statement after early pay | New, lower balances are what report |

| Remove an error | 30—45 days post-dispute CRA investigation window | |

| Add new card | Immediate small dip; 3—6 months stabilize | Inquiry + new line; age grows back |

| On-time streak | 3—12 months Payment history weight compounds with time | |

Tier Ladder

FoundationalBuild PhaseRevenue-Based ReadyBank-Ready

0–3940–6465–8485–100

Credit-Building Actions: What Your EIN-Only Approval Tier Means and What to Fix Next

Tiered Credit-Building Actions| Approval Tier | Current Signal | Likely Interpretation | Best Next Move |

|---|

| Foundational | Autopay minimums to eliminate late risk Identify statement cut dates; set early-pay reminders Keep per-card utilization under 9% | Autopay minimums to eliminate late risk Identify statement cut dates; set early-pay reminders Keep per-card utilization under 9% | Strengthen the next readiness signal before moving up. |

| Build Phase | Add 1 secured/entry card if thin; keep $0 lates for 6—12 months Maintain one small reporting balance; others $0 Space new applications 3—6 months apart | Add 1 secured/entry card if thin; keep $0 lates for 6—12 months Maintain one small reporting balance; others $0 Space new applications 3—6 months apart | Strengthen the next readiness signal before moving up. |

| Revenue-Based Ready | Optimize Request limit increases after 6—9 clean months Rotate spend to avoid single-card spikes Pair cards for category rewards without utilization drift | Optimize Request limit increases after 6—9 clean months Rotate spend to avoid single-card spikes Pair cards for category rewards without utilization drift | Strengthen the next readiness signal before moving up. |

| Bank Ready | Relationship Keep a checking/savings relationship to support internal underwriting Show steady deposits and low overdraft activity Prequalify with soft-pull channels before hard inquiries | Relationship Keep a checking/savings relationship to support internal underwriting Show steady deposits and low overdraft activity Prequalify with soft-pull channels before hard inquiries | Strengthen the next readiness signal before moving up. |

| Summary: The tier progression shows how the signal matures from basic setup into stronger approval readiness. Interpretation: Use the table to identify the weakest current signal and the cleanest next move before applying. |

Next move

Pick one utilization habit to fix this week: schedule early payments tied to your statement cut dates. Then add one positive: a small recurring bill on one card to keep healthy, low activity reporting.

For the broader readiness path, use the EIN-Only Approval Score™ and the Business Credit Optimization Checklist to connect this topic to your next approval move.

Sources