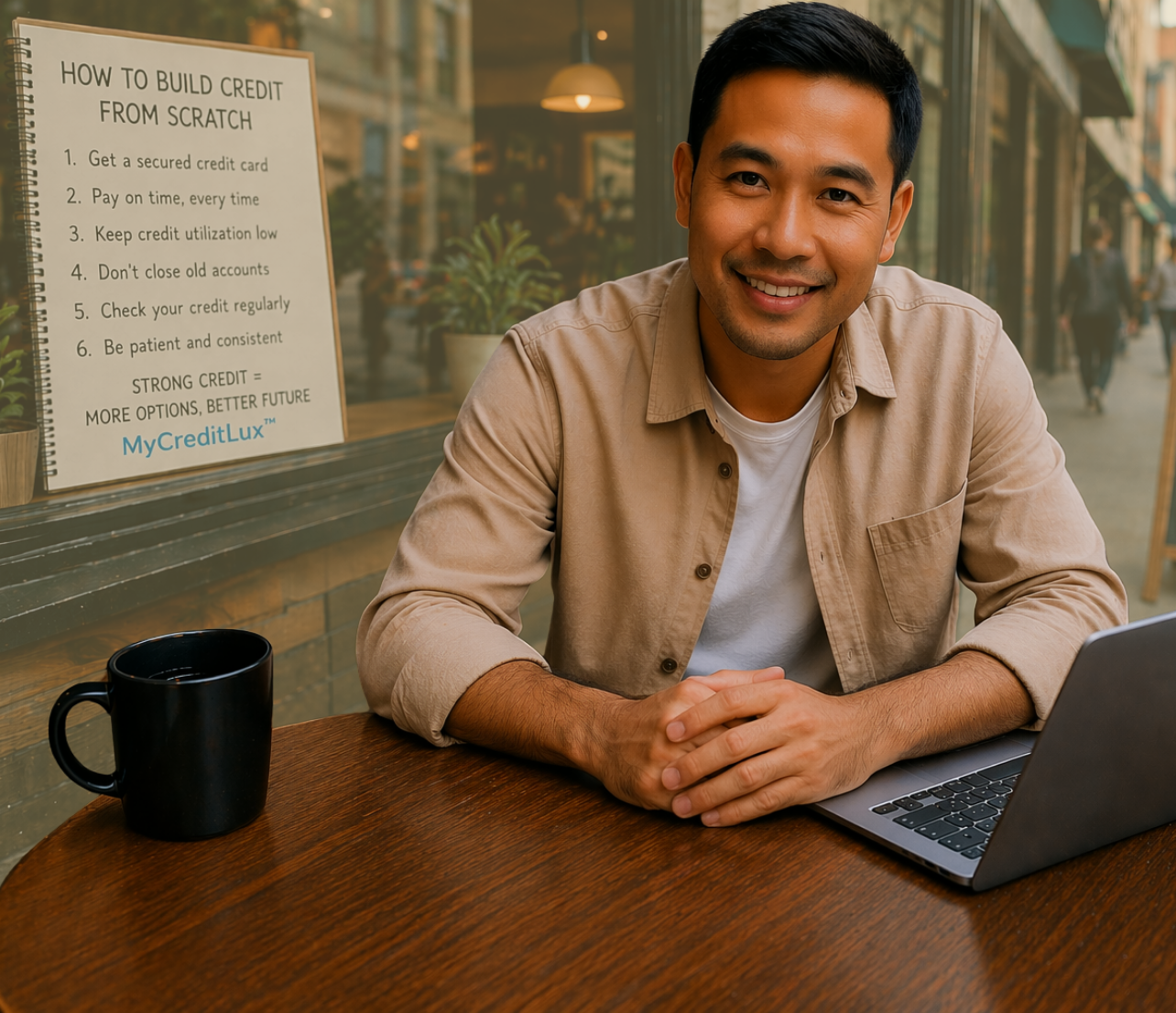

Key Takeaways

- You need reportable tradelines, not just activity, for a score to appear.

- One primary revolving line plus on-time payments builds scorable data within 1–3 months.

- Keep utilization under 10% of the limit; under 30% is acceptable if cash is tight.

- Avoid shotgun applications and junk products that don’t report to all bureaus.

- Time in file matters: 6 months to first reliable score, 12–24 months to look strong.

How lenders interpret a thin or no-file

Lenders look for signals they can price: verified identity, tradelines that report to Experian, Equifax, and TransUnion, and payment patterns across time. A no-file means they lack probability estimates, so approvals are limited or collateralized. A thin file (one to two tradelines) can be approved if risk controls are tight: low limits, higher APR, and stricter verification.

Your first moves that actually build

- Open one secured credit card or entry-level unsecured card that reports to all three bureaus. Fund a deposit if needed.

- Use it weekly for small, planned purchases you were making anyway.

- Pay on time, every time—set autopay for statement balance or at least minimum.

- Keep statement-date utilization under 10% for the cleanest score signal.

- After 90 days of clean reporting, consider one additional, high-quality tradeline if you still need depth.

Starter Credit Accounts That Actually Build| Account Type | Reports To | Best For | Risks / Watchouts |

|---|

| Secured Credit Card | All three bureaus (confirm before applying) | No file or thin file; predictable approval | Deposit required; avoid annual fees if possible |

| Entry-Level Unsecured Card | All three bureaus (prime issuers) | Thin file with solid income and low DTI | Low limit; watch for annual fees and high APR |

| Credit-Builder Loan (Installment) | All three bureaus (credit unions/fintech) | Adding mix after 3—6 months of revolving | Fees/interest; funds often locked until completion |

| Authorized User (AU) | Varies by issuer; verify AU reporting | Leveraging a trusted person's long, clean history | Backfires if primary has high utilization or lates |

Mechanics that move your score

Payment history drives the most weight, followed by utilization, age, mix, and new inquiries. Scores read snapshots on statement dates. A single late payment can suppress an emerging file for years; pristine data compounds quickly.

- Payment history: 35% weight—set autopay and calendar reminders.

- Utilization: 30%—keep below 10% on statement day; pay a mid-cycle amount if needed.

- Age: 15%—avoid closing your first good account.

- Mix: 10%—start with revolving; add an installment only if it fits a real need.

- New credit: 10%—space applications 90+ days; avoid same-day sprees.

Reporting and Scoring Timeline| Phase | What Happens | Your Move | Typical Time |

|---|

| Activation | New tradeline opens; identity matches | Enable autopay; make a small purchase | Week 0 |

| First Statement | Balance snapshot reported to bureaus | Keep utilization under 10% | Weeks 4—6 |

| Initial Score | Scoreable with enough history (model-dependent) | Stay consistent; avoid new apps | 1—3 months |

| Stability | Risk stabilizes; limits may grow | Ask for CLI or add one quality line if needed | 6—12 months |

| Prime Profile | Age and clean history strengthen approvals | Maintain low utilization; avoid closures | 12—24 months |

Common weak moves to skip

- Prepaid cards or debit activity—these don’t report as credit.

- Store cards you don’t need—often high APR and narrow utility.

- Multiple applications in a week—clusters of inquiries look riskier.

- Carrying a balance “for points”—interest costs you score and money.

- High utilization near statement date—your score reads the snapshot, not your intent.

Authorized user: when it helps, when it doesn’t

Authorized user status can add age and low utilization if the bank reports AU to all bureaus and the primary account is spotless. It won’t fix late payments or heavy utilization, and some score versions discount AU data when they suspect gaming.

Timeline and next steps

Expect 1–3 months to generate data visibility, ~6 months for a dependable FICO score, and 12–24 months for lenders to view your file as stable. Keep the first card open, layer a second quality line if needed, and let age work for you. Reassess limits after six on-time cycles.

Utilization Targets and Examples| Card Limit | 10% target 30% bound Tips 30%> | 30% bound Tips | Tips |

|---|

| $200 $20 $60 Pay mid-cycle if needed $60 $20 | | | |

| $500 $50 $150 Keep statement balance low $150 $50 | | | |

| $1,000 $100 $300 Autopay statement balance $300 $100 | | | |

| $2,000 $200 $600 Request higher limit after 6 on-time payments $600 $200 | | | |

Utilization Targets and Examples| Card Limit | 10% target 30% bound Tips 30%> | 30% bound Tips | Tips |

|---|

| $200 $20 $60 Pay mid-cycle if needed $60 $20 | | | |

| $500 $50 $150 Keep statement balance low $150 $50 | | | |

| $1,000 $100 $300 Autopay statement balance $300 $100 | | | |

| $2,000 $200 $600 Request higher limit after 6 on-time payments $600 $200 | | | |

Tier Ladder

FoundationalBuild PhaseRevenue-Based ReadyBank-Ready

0–3940–6465–8485–100

Credit-Building Moves: What Your EIN-Only Approval Tier Means and What to Fix Next

Credit-Building Moves by Tier| Approval Tier | Current Signal | Likely Interpretation | Best Next Move |

|---|

| Foundational | Open one secured or entry-level card that reports to all bureaus Autopay on; keep utilization under 10% No new apps for 90 days | Open one secured or entry-level card that reports to all bureaus Autopay on; keep utilization under 10% No new apps for 90 days | Strengthen the next readiness signal before moving up. |

| Build Phase | After 3 clean statements, consider one additional quality tradeline Ask for credit limit increase at month 6 Add credit-builder loan only if it fits a real need | After 3 clean statements, consider one additional quality tradeline Ask for credit limit increase at month 6 Add credit-builder loan only if it fits a real need | Strengthen the next readiness signal before moving up. |

| Revenue-Based Ready | Optimize rewards only after habits are stable Maintain aggregate utilization under 10% Monitor reports monthly for accuracy | Optimize rewards only after habits are stable Maintain aggregate utilization under 10% Monitor reports monthly for accuracy | Strengthen the next readiness signal before moving up. |

| Bank Ready | Establish a credit union or primary bank relationship Use prequalification before new apps Preserve oldest account to protect age | Establish a credit union or primary bank relationship Use prequalification before new apps Preserve oldest account to protect age | Strengthen the next readiness signal before moving up. |

| Summary: The tier progression shows how the signal matures from basic setup into stronger approval readiness. Interpretation: Use the table to identify the weakest current signal and the cleanest next move before applying. |

Advisor note

Here is the lender-view interpretation to keep in mind:

“

Strong credit from zero is about boring consistency: one clean line, low utilization, and on-time payments—repeated.

— Trice Odom, Credit & Consumer Finance Strategist, MyCreditLux™

For the broader readiness path, use the EIN-Only Approval Score™ and the Business Credit Optimization Checklist to connect this topic to your next approval move.

Sources