Why Credit Behavior Matters More Than Intent

Lenders and scoring models react to the actions recorded in your file—payments, balances, and timeliness—not your plans. Here’s how to align behavior with what underwriters actually read.

Personal credit is the financial system used to evaluate an individual’s borrowing reliability based on credit reports, credit scores, and account activity. Lenders rely on consumer credit data to assess financial risk, determine loan approvals, and establish borrowing limits.

The Personal Credit section of MyCreditLux™ explains how the consumer credit system works, including how credit reports are created, how scoring models interpret financial behavior, and how account activity influences lending decisions.

Understanding how this system operates helps explain why lenders approve or decline applications and how financial profiles develop over time.

The consumer credit system operates through a structured process that records financial activity, evaluates borrowing risk, and interprets financial behavior.

This process relies on three core components:

credit reporting

credit scoring models

credit account performance

Together, these elements form the foundation used by lenders to evaluate financial reliability.

Credit reporting is the process through which lenders submit financial activity to credit bureaus. These bureaus maintain detailed reports that document payment history, account balances, and other financial signals used to assess creditworthiness.

Explore the Credit Reporting section to understand how consumer credit reports are constructed and maintained.

Credit scores are numerical models designed to estimate the likelihood that a borrower will repay debt. These scoring systems analyze information from credit reports to evaluate financial behavior and predict lending risk.

The Credit Scores section explains how scoring models interpret utilization, payment reliability, and credit history.

Credit accounts—including credit cards, loans, and lines of credit—form the structural foundation of a consumer credit profile. The way these accounts are managed influences utilization levels, payment history, and overall borrowing risk.

The Credit Accounts and Behavior & Risk sections explain how account activity shapes financial outcomes.

Lenders and scoring models react to the actions recorded in your file—payments, balances, and timeliness—not your plans. Here’s how to align behavior with what underwriters actually read.

A lender reads patterns, not just a score. Learn the exact personal credit signals that increase or calm risk before an approval decision.

A high score predicts timely repayment; it does not prove wealth, durable cash flow, or low financial stress. Learn how to read the signal without overreading it.

How People Confuse Credit With Financial Strength Read More »

Credit measures repayment reliability and loss risk, not your worth. Learn how lenders read your behavior and what to do next to strengthen your signal.

Available credit isn’t static. It shifts with authorizations, posting, holds, refunds, and payments—especially around your statement close and due date.

How Available Credit Changes Throughout the Month Read More »

Credit and cash both pay for things, but only credit creates a reportable record that lenders score. Understand the mechanisms, costs, protections, and next steps so you choose with intent.

A credit profile is the full record lenders read—accounts, limits, age, utilization, payment history, derogatories, and inquiries—not just a score. Learn how it’s interpreted and what to fix first.

Two people can earn the same amount yet see very different approvals, limits, and rates. Here’s how profile structure, reporting, and lender interpretation create the gap—and how to close it.

Why Two People With the Same Income Can Have Different Credit Outcomes Read More »

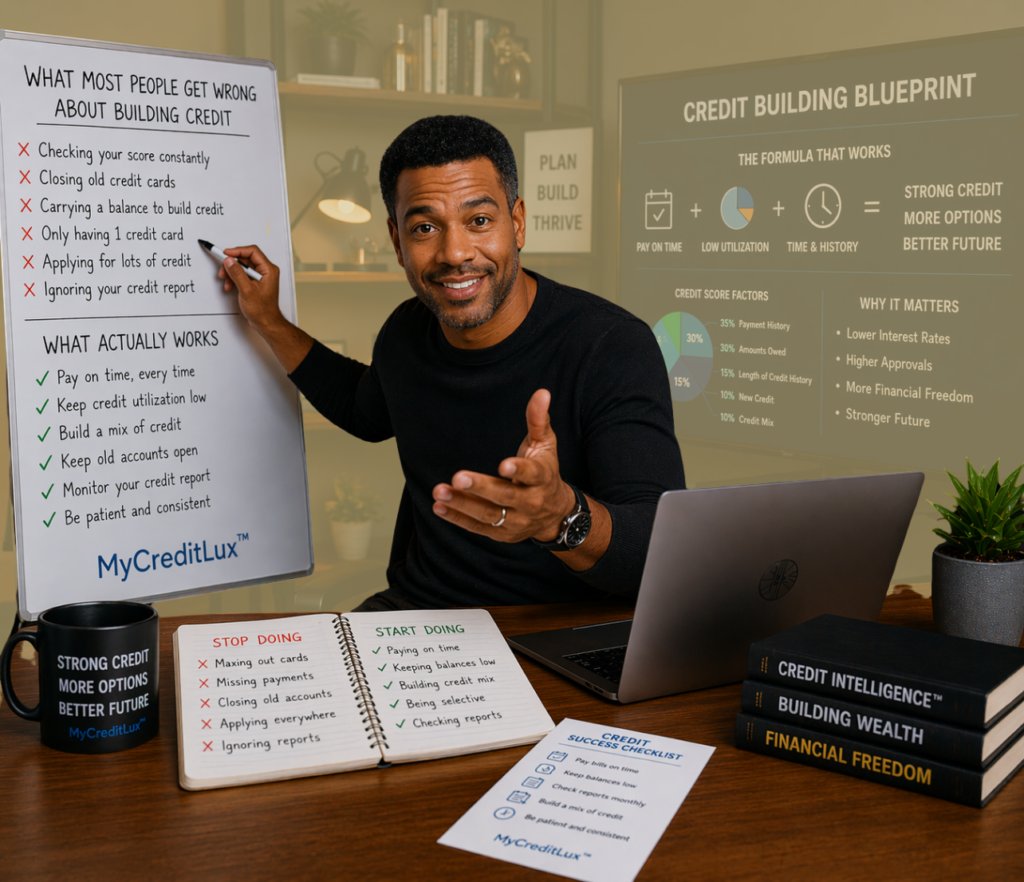

Most credit advice fails because it ignores how data is reported and how lenders interpret risk. Fix the five biggest misconceptions and build momentum that sticks.

The first moves you make with credit set your baseline. Avoid these early mistakes to keep scores stable, reports clean, and approvals easier later.

Common Personal Credit Mistakes at the Beginning Read More »